I have made my case, on this thread and others that you disagree with....that is fine.

My point about going around in circles debating it is for several reasons.

You have your beliefs, I have mine, we both believe that we have the burden of proof on our side.

Studies have shown, when it comes to political beliefs that even when presented with the truth, with factual information that can be backed up, those beliefs supersede said facts.

In fact they have shown that instead of come to the conclusion that they were indeed wrong about their beliefs and statements, that people actually "double-down" on their views instead of admitting they are wrong.

You are once again, free to believe what you wish...so far, we are still free to do that.

And once again, like I stated in the original statement for this thread - I don’t wish this to be a debate thread...disagree all you want, but that was not the intended point.

I have no doubt that I will NOT sway you to hold the same beliefs that I do...nor should you about me.

I know that there will always be those who disagree with what I have to say...and you in turn, should realize that too...it doesn’t make either side more ignorant, we have only been presented differing facts and have drawn our own conclusions based on those and most likely how we have lived our lives and the influences in them.

I don’t have to be right all the time, to all people...nor will I waste my time trying...there will always be a voice of opposition.

I have made my case, on this thread and others that you disagree with....that is fine.

My point about going around in circles debating it is for several reasons.

You have your beliefs, I have mine, we both believe that we have the burden of proof on our side.

Studies have shown, when it comes to political beliefs that even when presented with the truth, with factual information that can be backed up, those beliefs supersede said facts.

In fact they have shown that instead of come to the conclusion that they were indeed wrong about their beliefs and statements, that people actually "double-down" on their views instead of admitting they are wrong.

You are once again, free to believe what you wish...so far, we are still free to do that.

And once again, like I stated in the original statement for this thread - I don’t wish this to be a debate thread...disagree all you want, but that was not the intended point.

I have no doubt that I will NOT sway you to hold the same beliefs that I do...nor should you about me.

I know that there will always be those who disagree with what I have to say...and you in turn, should realize that too...it doesn’t make either side more ignorant, we have only been presented differing facts and have drawn our own conclusions based on those and most likely how we have lived our lives and the influences in them.

I don’t have to be right all the time, to all people...nor will I waste my time trying...there will always be a voice of opposition.

That's a bit of a weird post, kind of "I respect your right to be wrong" and, like I've said to other posters and on other points, singularly unpersuasive.

Although you seem to be saying you dont aim to be persuasive either, just to present information, which you dont want to be discussed, or at the very least dont want to be debated.

Have you thought about how what you've said about doubling down in beliefs against the evidence could equally apply to your self as others?

No, I meant cynicism.

That is how it appears to be anyhow...perhaps I am wrong, I never claimed to be right.

I am pretty sure that I inferred that I was, indeed a sales rep for a giant corporation at one time.

The Ãœber-rich are already looking for ways to gain more profit...take our recent Supreme Court Decisions squarely handing over electoral power to the Ãœber-rich.

This is nothing but a scheme to further their political clout without the need for lobbyists...it’s so much easier to be beholden to someone and call in that favor.

You know, I never intended this to be a debate thread...I can go back and forth with you but that was not the point.

I am looking for constructive answers and thoughts on actions that can be taken.

If you disagree with the politics that I have to offer then you are free to start your own thread.

Hmm, yeah, you dont like discussion, I've sort of grasped that and these threads are about validation. That's alright, my mistake and we dont need to talk. Have a nice day

Hmm, yeah, you dont like discussion, I've sort of grasped that and these threads are about validation. That's alright, my mistake and we dont need to talk. Have a nice day

That's a bit of a weird post, kind of "I respect your right to be wrong" and, like I've said to other posters and on other points, singularly unpersuasive.

Although you seem to be saying you dont aim to be persuasive either, just to present information, which you dont want to be discussed, or at the very least dont want to be debated.

Have you thought about how what you've said about doubling down in beliefs against the evidence could equally apply to your self as others?

Hmm, yeah, you dont like discussion, I've sort of grasped that and these threads are about validation. That's alright, my mistake and we dont need to talk. Have a nice day

I am fully aware that I could be doubling down my own beliefs...I would not have said it otherwise.

And I never said that I was not out to persuade anyone at all...I hope that I do to a certain extent through the presentation of what I post on this thread.

I don’t mind having discussions either...but the way you discuss things is wholly singular...I don’t know if you even realize you do it or not, but you kind of come across as condescending.

That doesn’t make me want to debate, nor discuss, nor feel open-minded and have the possibility to be persuaded by what you are saying...perhaps this is only me and it has nothing to do with you...I really couldn’t say for sure Lark.

Maybe it is all just in my head...I never professed to know it all...the things I post are things which I find important in my life and I feel a certain level of passion for...if my emotions get the best of me at times (and I know that they can and do) then I apologize.

I do want things discussed...I do like discussions...but if you come here to debate and discuss while throwing underhanded jabs at those who have a different viewpoint than you then it becomes pointless.

It is like debating the Bible with my good pal LucyJr...I don’t debate him for two reasons - I respect him as my friend and do not wish to demean his personal spiritual beliefs...and...his beliefs are his own and he feels very strongly about them...it would be like two people living on earth...one can see color and one cannot...and each not believing that the other can indeed see things differently. And a step further than that, neither one is correct in assuming that their vision is more important because of it.

It isn’t that I cannot debate you Lark...I used to debate on this forum until my fingers were numb...I dislike to now because people do not have an open point of view...their beliefs are basically set in stone, especially by the time we are in our 30’s like you and I are.

And so you go round and round...it becomes a pointless dance to see who is right and who is wrong...I don’t need to be right Lark...I don’t want to waste time debating why what I post is worthwhile....I think people should be free to read what is presented and make up their own mind....you either agree or you don’t agree...you can even explain why you feel that way, and I will even counterpoint once or twice...but I cannot stand the forever back and forth where neither side has any “give”.

Princeton study concludes: US is an oligarchy, not a democracy

In a recent report from the academic journal Perspectives on Politics, the United States is not a democracy, but is instead, an oligarchy. For those who aren’t up with fancy words, this means that the US government is very, very corrupt.

The news: A new scientific study from Princeton researchers Martin Gilens and Benjamin I. Page has finally put some science behind the recently popular argument that the United States isn’t a democracy any more. And they’ve found that in fact, America is basically an oligarchy. An oligarchy is a system where power is effectively wielded by a small number of individuals defined by their status called oligarchs. Members of the oligarchy are the rich, the well connected and the politically powerful, as well as particularly well placed individuals in institutions like banking and finance or the military. For their study, Gilens and Page compiled data from roughly 1,800 different policy initiatives in the years between 1981 and 2002. They then compared those policy changes with the expressed opinion of the United State public. Comparing the preferences of the average American at the 50th percentile of income to what those Americans at the 90th percentile preferred, as well as the opinions of major lobbying or business groups, the researchers found out that the government followed the directives set forth by the latter two much more often.

It’s beyond alarming. As Gilens and Page write, “the preferences of the average American appear to have only a minuscule, near-zero, statistically non-significant impact upon public policy.” In other words, their statistics say your opinion literally does not matter. This problem has been steadily escalating for four decades. While there are some limitations to their data set, economists Thomas Piketty and Emmanuel Saez constructed income statistics based on IRS data that go back to 1913. They found that the gap between the ultra-wealthy and the rest of us is much bigger than you would think, as mapped by these graphs from the Center On Budget and Policy Priorities:

Piketty and Saez also calculated that as of September 2013 the top 1% of earners had captured 95% of all income gains since the Great Recession ended. The other 99% saw a net 12% drop to their income. So not only is oligarchy making the rich richer, it’s driving policy that’s made everyone else poorer.

What kind of oligarchy?

As Gawker’s Hamilton Nolan explains, Gilens and Page’s findings provide support for two theories of governance: economic elite domination and biased pluralism. The first is pretty straightforward and states that the ultra-wealthy wield all the power in a given system, though some argue that this system still allows elites in corporations and the government to become powerful as well. Here, power does not necessarily derive from wealth, but those in power almost invariably come from the upper class. Biased pluralism on the other hand argues that the entire system is a mess and interest groups ruled by elites are fighting for dominance of the political process. Also, because of their vast wealth of resources, interest groups of large business tend to dominate a lot of the discourse. In either case, the result is the same: Big corporations, the ultra-wealthy and special interests with a lot of money and power essentially make all of the decisions. Citizens wield little to no political power. America, the findings indicate, tends towards either of these much more than anything close to what we call “democracy” – systems such as majoritarian electoral democracy or majoritarian pluralism, under which the policy choices pursued by the government would reflect the opinions of the governed.

Nothing new:

And no, this isn’t a problem that’s the result of any recent Supreme Court cases – at least certainly not the likes FEC v. Citizens United or FEC v. McCutcheon. The data is pretty clear that America has been sliding steadily into oligarchy for decades, mirrored in both the substantive effect on policy and in the distribution of wealth throughout the U.S. But cases like those might indicate the process is accelerating.

Scott Neeson, former head of 20th Century Fox International left Hollywood to save children rotting in Cambodia's garbage dumps

He sold his mansion, Porsche, and yacht to set off for Cambodia to provide food, shelter and education to destitute children. Scott now cares for more than 1,000 Cambodian children and their families.

Are you talking about the referendum by the crimean people in which they chose to join russia rather than the EU to avoid being massively and unpayably indebted to the IMF as the unelected kiev government wants them to be?

I would let the people in the Ukraine make their own mind up like the russians have done

I think the people in the east and other parts should be allowed a vote as well to decide which side they join. If i lived there i would want a vote...and i'd vote to join russia because russia is part of the up and coming BRICS block of countries and is better placed to ride out the coming economic crisis because the BRICS countries are laden with gold which can back the new currency that will replace the dollar when it collapses as the world reserve currency

I'd make sure everyone in the US understood how the banking system worked and what their REAL history as a country is which is to say a constant struggle between the rights of the people against the international bankers who have sought to create a central bank through which they can control the economy; they finally acheived their aim with the creation of the federal reserve in 1913

So i would end the fed. I would put the power to print money and control the money supply back in the hands of the treasury and out of the hands of the private bankers

I would create a council to oversee all reforms and i would put certain people on this council. These people don't agree on everything but i think a certain synthesis would come out of their melting pot of ideas. I would include people like Prof. Michael Hudson and Prof. David Graeber to help oversee a debt jubilee and a write down of the debts to the ability to pay to ensure that NO homeowners lost their homes but rather that the global investors lost some of their ridiculous fortunes

I would re-instate the Glass-Steagal Act

I would end corporate personhood

I would tax the wealthy to take back all the missapropriated funds and create new banks along the lines of the North Dakota bank; I would let the zombie 'too big to fail' banks fail

I would write down the debts to the abilty to pay (see above)

I would use RICO laws to break up all the big corporations and provide incentives for small to medium sized businesses

I would jail the bankers involved in all the scandals, end the derivatives market and work towards a global consensus on ending all the tax havens

I would end all hostilities in the middle east by withdrawing funding to Israel thereby bringing Israel to the negotiation table. I would chair a publically televised negotiation between the israelis and the palestineans to find out what each side wants and to find a compromise between the two. Israelis need security and Palestineans need a viable land with access to their natural resources so that they can have a sustainable future for their youth. I would bring Palestine into the UN and recognise their nationhood

I would end alliances with autocratic middle eastern leaders (stop selling them weapons) and instead pursue a policy of homegrown renewable energies

I would reach out to Russia and China to construct the least turbulent path forward for the global community in terms of sharing the worlds resources and in terms of a global currency moving forward, pull back all the US military bases, slash spending on the military and work with the other global powers towards nuclear dissarmament

ENERGY is the key so to achieve much of the above viable energy alternatives to middle eastern oil would need to be explored and adopted. However by breaking the power of the global energy cartel this would open the doors to that process

Yes i would create an advisory board and fill it with all my heros! This council would create proposals and publicise them to the public in an open forum. Referendums would be held on each issue to ensure the people understood the proposals and the implications and then could either yay or nay them

The council would not just be concerned with economic matters but also matters of civil liberties and i'd get people like Chris Hedges, Glenn Greenwald, Julian Assange and Daniel Ellsberg on board to help dismantle the surveillance state and to ensure a free press and the end of the NDAA

As the US ended its aggressive foreign policy it would have less enemies abroad and would require less security. As standards of living rose at home there would be less need for security against homegrown threats

I would use the internet to reach as many people as i could. A website would show the televised meetings and i would make every step of the process open and transparent

It would be important that the public knew what was being proposed and also that they agreed with it before changes were carried out

The website would therefore have several functions. Firstly to formulate, discuss and debate the reforms, secondly to put the reforms to the public, thirdly to facilitate the referendum on each reform and finally to track the ongoing process in order to monitor the impact of reforms and to manage any externalities or unforeseens...a fluid and dynamic process that kept at every turn the well being of the public in mind at all times

The creation of a new interest free currency created and controlled by the treasury

Once renewables were in place they would enable subsidised energy bills for the public which would free up more money to be spent into the real economy

A grab of the funds of the banking cartel......in the same way that police can seize the ill gotten gains of criminals the government should seize the assets of the criminal banking fraternity

Ideas such as 100% tax on earnings above $1 billion might provide a lot of funds!

I don’t get what you are getting at?

Those are not my decisions to make currently, and thank god for that.

Making decisions about Crimea and the Cuban Missile Crisis would have to be based upon a lot of knowledge that is not public...so I cannot give you a very knowledgable answer.

Which trash are we speaking of? Wall Street trash? I would set up a regulatory commission with big fucking teeth that wasn’t tied to Wall Street and the FEC (many of whom go and work on Wall Street after leaving the FEC), I wouldn’t just fine the companies, people would see jail time, not country club jail, - prison.

I seek the guidance of those who are more experienced when I need guidance from someone more experienced.

We would meet at - Chili’s? *shrug*

I would pay for it with the tax breaks that we are giving multi-billion dollar profit making corporations and the scaled back the US war machine to a level that isn’t out of it’s mind like it is now. That could easily pay for what needs to get done.

Less, war expenditures.

Fewer tax-breaks for millionaires and billionaires, and for giant billion-dollar profit making corporations...they are NOT the job creators...if they were we would be swimming in jobs by now...they are the money hoarders...and hoarding money doesn’t do our economy any good at all. The middle/working class spending money is what drives the economy....if it continues on the way it is going that money is going to eventually dry up...then what? It’s gonna hit the fan is what.

This came out in the news just yesterday....how sad....

The Koch brothers are going after solar panels

The conservative solar blowback has arrived in full force

David Koch(Credit: AP/Phelan M. Ebenhack)

Homeowners and businesses that wish to generate their own cheap, renewable energy now have a force of conservative political might to contend with, and the Koch brothers are leading the charge. The L.A. Times, to its credit, found the positive spin to put on this: Little old solar “has now grown big enough to have enemies.”

The escalating battle centers over two ways traditional utilities have found to counter therapidly growing solar market: demanding a share of the power generated by renewables and opposing net metering, which allows solar panel users to sell the extra electricity they generate back to the grid – and without which solar might no longer be affordable.

The Times reports on the conservative heavyweights making a fossil fuel-powered effort to make those things happen:

The Koch brothers, anti-tax activist Grover Norquist and some of the nation’s largest power companies have backed efforts in recent months to roll back state policies that favor green energy. The conservative luminaries have pushed campaigns in Kansas, North Carolina and Arizona, with the battle rapidly spreading to other states.

…The American Legislative Exchange Council, or ALEC, a membership group for conservative state lawmakers, recently drafted model legislation that targeted net metering. The group also helped launch efforts by conservative lawmakers in more than half a dozen states to repeal green energy mandates. “State governments are starting to wake up,” Christine Harbin Hanson, a spokeswoman for Americans for Prosperity, the advocacy group backed by billionaire industrialists Charles and David Koch, said in an email. The organization has led the effort to overturn the mandate in Kansas, which requires that 20% of the state’s electricity come from renewable sources.

“These green energy mandates are bad policy,” said Hanson, adding that the group was hopeful Kansas would be the first of many dominoes to fall. The group’s campaign in that state compared the green energy mandate to Obamacare, featuring ominous images of Kathleen Sebelius, the outgoing secretary of Health and Human Services, who was Kansas’ governor when the state adopted the requirement.

What’s especially disappointing is that for a while now, we’ve been hearing about how solar power is actually gaining traction in red states, with conservatives switching the focus from that liberal scourge, renewable energy, to something their base hates even more: taxes. Even Barry Goldwater Jr. has spoken out against the idea of allowing utilities to charge a monthly fee to the owners of rooftop solar panels, or what he and other advocates refer to as a “solar tax.”

At Mother Jones, Kevin Drum bemoans the resurgence of knee-jerk opposition to solar:

There are dozens of good reasons that we should be building out solar as fast as we possibly can–plummeting prices, overdependence on foreign oil, poisonous petrostate politics, clean air–but yes, global warming is one of those reasons too. And since global warming has now entered the conservative pantheon of conspiratorial hoaxes designed to allow liberals to quietly enslave the economy, it means that conservatives are instinctively opposed to anything even vaguely related to stopping it. As a result, fracking has become practically the holy grail of conservative energy policy, while solar, which improves by leaps and bounds every year, is a sign of decay and creeping socialism.

Compared to that, even Goldwater’s insistence that utilities are anti-free market (“Choice means competition. Competition drives prices down and the quality up. The utilities are monopolies. They’re not used to competition. That’s what rooftop solar represents to them”) may not be enough to sway the rhetoric back in solar’s favor.

Why Economist Thomas Piketty Has Scared the Pants Off the American Right

If you call rigorous economic research on inequality a Communist plot, will it go away?

Thomas Piketty is no radical. His 700-page book Capital in the 21st Centuryis certainly not some kind of screed filled with calls for class warfare. In fact, the wonky and mild-mannered French economist opens his tome with a description of his typical Gen X abhorrence of what he calls the “lazy rhetoric of anticapitalism." He is in no way, shape, or form a Marxist. As fellow-economist James K. Galbraith has underscored in his review of the book, Piketty "explicitly (and rather caustically) rejects the Marxist view" of economics.

But he does do something that gives right-wingers in America the willies. He writes calmly and reasonably about economic inequality, and concludes, to the alarm of conservatives, that there is no magical force that drives capitalist societies toward shared prosperity. Quite the opposite. He warns that if we don't do something about it, we may end up with a society that is more top-heavy than anything that has come before – something even worse than the Gilded Age.

For this, in America, you get branded a crazed Communist by the right. In this past weekend'sNew York Times, Ross Douthat sounds the alarm in an op-ed ominously tited "Marx Rises Again." The columnist hints that he and his fellow pundits have only pretended to read the book but nevertheless feel comfortable making statements like "Yes, that’s right: Karl Marx is back from the dead" about Piketty. The National Review's James Pethokoukis joins in the games with a silly article called "The New Marxism" in which he repeats the nonsense that Piketty is some sort of Marxist apologist.

For Douthat and his tribe, the proposition that unfettered capitalism marches toward gross inequality is not a conclusion based on carefully collected data, strenuous research and a sweeping view of history. It has to be a Communist plot.

The very heft of Piketty's book is terrifying to the Douthats, and no wonder they don't dare to read it, because if they did, they would find chart after chart, data set after data set, and hundreds of years worth of economic history scrutinized.

Income and wealth inequality have not been comprehensively studied to date, which has to do with the paucity of historical data and the difficulties of making comparisons between countries and populations when there are so many variables. Piketty's contribution is to painstakingly comb over the available data and illuminate trends that would leave no reasonable person in doubt of the fact that capitalism's inherent dynamics create inequality, and that only our express intervention, in the form of things like a global wealth tax, investment in skills and training, and the diffusion of knowledge can lead us to a different outcome.

To the horror of conservatives, the public is rushing out to buy this weighty economic treatise: the book is #1 on Amazon and has hit the New York Timesbestseller list. A public that not only inuits conservative economic nonsense but has the detailed information to back up that gut instinct is just too awful for words.

Piketty is scaring the right because he is a serious researcher and a calm, disciplined observer who writes in measured tones. But for conservatives who have based the last several decades of economic discussion on mythology, this dose of reality has come at them like a chillling blast of Arctic air.

Let them have their hysteria. It's a testimony to the utter bankruptcy of their ideas.

Memo to liberals and progressives: making Piketty into a rock star isn't helping, either. Let's let the facts speak for themselves.

Matt Taibbi's New Book Is a Striking Study of How the Rich Are Never Punished for Their Crimes

'The Divide' is a riveting account of how the 1% get away with pretty much whatever they want.

Matt Taibbi has come a long way since the 1990s, when he co-edited a riotous expatriate newspaper in Moscow. For five years, Taibbi churned out the Gonzo, Slavic style, mixing satire and pranks with scathing opinion and analysis. Although he also played in the Mongolian Basketball Association, his time abroad wasn’t all fun and games. In the early 1990s, the Russian government began auctioning off shares of state enterprises, which Taibbi described as “the biggest thefts in the history of the human race.” He noted the calamitous effects of privatization on average Russians and scorned the American consultants who descended on Moscow to coordinate the auction. “Looking at their bright, happy faces,” Taibbi wrote, “you’d never guess that these were the people who’d had the balls to tell millions of Russians that their jobs and benefits needed to be sacrificed for the sake of ‘competitiveness.’ ”

Rather than lament the evils of neoliberalism, Taibbi chose to mock the carpetbaggers. “There was no point in fighting fair against people like this,” he claimed in his first co-authored book, “The Exile: Sex, Drugs, and Libel in the New Russia” (2000). “Humorless lefties like Ralph Nader had been doing that for decades, much more effectively and with greater attention than we ever could, to very little result.” He decided to “loathe the corporate henchmen not for what they did, but for who they were.” His goal was to “embarrass them socially, pick on their looks and their mannerisms and speech, expose them as people.”

In 2002, Taibbi returned to the United States with his attitude intact. When an alternative weekly hired him to cover the 2004 Democratic primaries, he struggled to find a satisfactory way to report on the absurdities he witnessed. He began showing up for work on mushrooms or in a gorilla suit; at one point, he played the hunger artist, forgoing food for a week and taking careful notes on what the other reporters were ingesting. Toward the end of his fast, he dropped two hits of acid, donned a Viking costume and tried to interview a campaign staffer.

Again, the Gonzo influence was unmistakable. Taibbi’s first solo book, “Spanking the Donkey: On the Campaign Trail With the Democrats” (2005), was an updated version of Hunter Thompson’s “Fear and Loathing: On the Campaign Trail ’72,” which was praised as the least factual and most accurate account of that presidential race. Taibbi even itemized the contents of his car trunk, as Thompson did at the beginning of “Fear and Loathing in Las Vegas.” It was therefore fitting that Rolling Stone magazine, which helped make Thompson a cultural icon, hired Taibbi as a contributing editor.

In his next book, “Griftopia: Bubble Machines, Vampire Squids, and the Long Con That Is Breaking America” (2010), Taibbi broadened his attack on high finance. One of his targets was former Federal Reserve Chairman Alan Greenspan, whom business reporters had long revered. When the stock bubble popped in 1999, Time magazine cast Greenspan as a member of the “Committee to Save the World.” Taibbi felt no such reverence; in fact, he regarded the Fed chair’s penchant for deregulation, low interest rates and Wall Street bailouts as an important source of the bubble in the first place. Characteristically, Taibbi made his critique personal. Greenspan was a “gnomish bug-eyed party crasher” who “flattered and bullshitted his way to the top,” and then turned the Federal Reserve into “a permanent bailout mechanism for the super-rich.” But Taibbi did more than impugn his targets; he also explained the intricacies of Wall Street’s labyrinthine hustles to general readers. That combination of bombast and clear explication made his claims increasingly difficult to ignore or refute.

Eventually the SEC and Justice Department began to stir. The same year “Griftopia” appeared, Goldman Sachs paid $550 million to settle charges that it misled investors about a subprime mortgage product. It was the largest SEC penalty ever paid by a single firm. Two years later, Citigroup paid $590 million to settle similar claims, and last year, JPMorgan Chase settled with the Justice Department for $13 billion, including a $3 billion penalty for its role in selling low-quality mortgage-backed securities. Despite the immense scale of the subprime grift, none of the major offenders faced criminal prosecution.

The Goldman Sachs story dramatically raised Taibbi’s media profile. But where would he go next? Given the government’s refusal to prosecute Wall Street bankers, it was perhaps natural that he would turn his attention to the legal system. In his latest book, “The Divide: American Injustice in the Age of the Wealth Gap,” Taibbi explores why Wall Street bankers are seemingly exempt from criminal prosecution, even as New York City targets petty crime – much of it manufactured by police in minority neighborhoods – more aggressively than ever. He cites statistics to make his argument, but mostly he reports on specific cases. One involves a working-class black man who finally decided to fight a misdemeanor charge for blocking pedestrian traffic – that is, standing on the sidewalk in front of his home. Taibbi also considers the zeal with which government agencies investigate and humiliate welfare recipients and undocumented residents for trying to provide for their families during hard times – times made all the harder because of unprosecuted crimes at the top of the economic food chain.

Everyone knows the rich receive special treatment in this country, especially in court. But Taibbi concludes that the government now offers a sliding scale of civil and criminal protection to U.S. residents. At one end of the spectrum, the very rich are virtually beyond accountability, no matter how massive and destructive their crimes may be. At the other end, the nation’s most vulnerable residents face unremitting investigation and prosecution by bureaucracies determined to find them guilty of something.

Taibbi also surfaces a new set of targets: Justice Department prosecutors who seek settlements for even the most outrageous white-collar scams. Many of them are recruited from law firms whose clients include the largest Wall Street banks. Lanny Breuer, who headed the department’s criminal division when the financial meltdown occurred, is Taibbi’s poster boy for this conflict of interest. Both he and Attorney General Eric Holder were partners at Covington & Burling, which represents JPMorgan Chase, Bank of America, Citigroup and Wells Fargo. All too often, Taibbi argues, the prosecutors have continued to behave like defense attorneys. When Holder was a Clinton administration official, for example, he wrote a memo arguing that prosecutors should consider “collateral consequences” when determining whether to charge persons or corporations. If a criminal prosecution would unduly harm innocent shareholders and employees, the logic went, it made more sense to settle. But once bankers realized they were beyond criminal prosecution, the incentives to transgress increased dramatically.

Taibbi illustrates the Justice Department’s “complete regulatory surrender” by briefly recounting the Hong Kong and Shanghai Banking Corporation case of 2012. HSBC admitted to laundering billions of dollars for Mexican and Colombian drug cartels, accepting $500,000 per day from Russian mobsters, working with banks connected to al-Qaida and facilitating deals with the sanctioned state of Iran. At a news conference, Breuer proudly announced that HSBC would pay a fine of $1.9 billion – less than 10 percent of that bank’s earnings for a single year. “I don’t think the bank got off easy,” Breuer said. A dubious Forbes magazine asked, “What’s a bank got to do to get into some real trouble around here?” The New York Times agreed: “Clearly, the government has bought into the notion that too big to fail is too big to jail.”

It got worse. When Swiss banking giant UBS was nailed for rigging Libor rates, which affected the price of trillions of dollars worth of financial products, Breuer lamely defended the $1.5 billion settlement at a news conference before Holder stepped in. “I’m not talking about just this case,” Holder said, “but in others we have resolved, the impact on the stability of financial markets around the world is something that we take into consideration.”

As with the Goldman Sachs story, other journalists have confirmed Taibbi’s major claims. Writing for Salon, David Dayen called attention to an article in American Lawyer that congratulated Covington & Burling for allowing its banking clients to escape justice “with very little damage.” One client “got off with just a $5 million fine,” while another “was fined just $75,000” for allegedly misleading investors about the firm’s subprime exposure. The article even quoted Breuer, who returned to Covington & Burling after his stint in the Justice Department. “Marrying regulatory expertise with white-collar lawyers is an extraordinary advantage,” Breuer said. For Dayen, the American Lawyer piece was a teachable moment. “Ex-regulators like Lanny Breuer can make millions defending the clients they used to regulate,” he wrote. “And with few exceptions, it’s all perfectly legal. We just don’t usually get to see the scheme displayed so obviously and transparently as it is in these marketing materials.”

In her New York Times column, Gretchen Morgenson also highlighted the Justice Department’s kid-gloves approach to Wall Street fraud. Citing a report by the department’s own inspector general, Morgenson noted that the FBI ranked complex financial crimes as the lowest priority of the six criminal threats within its area of responsibility. Moreover, the same report ranked mortgage fraud as the lowest threat within the complex financial crimes category. That report, Georgetown law professor Adam Levitin said, “confirmed what’s been clear for quite a while – that the D.O.J. has never taken mortgage fraud seriously.” Breuer declined to comment for Morgenson’s piece, but former Delaware Sen. Edward Kaufman, who now teaches law at Duke University, was more forthcoming. “The report fits a pattern that is scary for a democracy, that there really are two levels of justice in this country, one for the people with power and money and one for everyone else,” Kaufman said. “And that eats at the heart of what I think makes this country great.”

“The Divide” marks a shift in Taibbi’s tone. More Lincoln Steffens than Hunter Thompson, Taibbi drops most of the histrionics to reveal the corruption and injustice at hand. He even goes out of his way to be reasonable. He acknowledges that prosecuting financial cases can be expensive and risky, especially when the alleged crimes are complex and the defendants have vast legal resources at their disposal. That fact motivates prosecutors to settle such cases rather than try them in criminal court. He also concedes that many disadvantaged neighborhoods may benefit from tough policing. But he maintains that when combined, the two law-enforcement strategies add up to a glaring injustice. He also notes that it’s far too easy to introduce jurisdictional complications in financial cases that would never be allowed in less consequential cases. To make that point, he recounts a horrific case in which high-profile Wall Street financiers escaped punishment after trying to destroy a company they bet against as well as harassing its executives and their family members.

Taibbi’s is an important voice, especially in today’s media ecology. Support for investigative reporting has never been a given; when it comes to muckraking, you take it where you can get it. Taibbi has shown that he can deliver the goods, and “The Divide” is his most important book-length contribution to date. One wonders what the future holds for him. Inebruary, he announced he was leaving Rolling Stone to join First Look Media, where his website will feature investigative stories with a satirical edge. In describing his new venture, he linked his Russian experience to his current interests. “There was a certain kind of corruption that I got to see up close in the ’90s,” he said, “and I think that a version of it is being repeated here in the United States.”

Robert Reich: How to Fix Sky-high CEO Pay in Companies that Pay Workers Like Serfs

A new tax would narrow pay discrepancy–and help the economy.

Until the 1980s, corporate CEOs were paid, on average, 30 times what their typical worker was paid. Since then, CEO pay has skyrocketed to 280 times the pay of a typical worker; in big companies, to 354 times.

Meanwhile, over the same thirty-year time span the median American worker has seen no pay increase at all, adjusted for inflation. Even though the pay of male workers continues to outpace that of females, the typical male worker between the ages of 25 and 44 peaked in 1973 and has been dropping ever since. Since 2000, wages of the median male worker across all age brackets has dropped 10 percent, after inflation.

This growing divergence between CEO pay and that of the typical American worker isn’t just wildly unfair. It’s also bad for the economy. It means most workers these days lack the purchasing power to buy what the economy is capable of producing – contributing to the slowest recovery on record. Meanwhile, CEOs and other top executives use their fortunes to fuel speculative booms followed by busts.

Anyone who believes CEOs deserve this astronomical pay hasn’t been paying attention. The entire stock market has risen to record highs. Most CEOs have done little more than ride the wave.

There’s no easy answer for reversing this trend, but this week I’ll be testifying in favor of a bill introduced in the California legislature that at least creates the right incentives. Other states would do well to take a close look.

The proposed legislation, SB 1372, sets corporate taxes according to the ratio of CEO pay to the pay of the company’s typical worker. Corporations with low pay ratios get a tax break.Those with high ratios get a tax increase.

For example, if the CEO makes 100 times the median worker in the company, the company’s tax rate drops from the current 8.8 percent down to 8 percent. If the CEO makes 25 times the pay of the typical worker, the tax rate goes down to 7 percent.

On the other hand, corporations with big disparities face higher taxes. If the CEO makes 200 times the typical employee, the tax rate goes to 9.5 percent; 400 times, to 13 percent.

The California Chamber of Commerce has dubbed this bill a “job killer,” but the reality is the opposite. CEOs don’t create jobs.Their customers create jobs by buying more of what their companies have to sell – giving the companies cause to expand and hire.

So pushing companies to put less money into the hands of their CEOs and more into the hands of average employees creates more buying power among people who will buy, and therefore more jobs.

The other argument against the bill is it’s too complicated. Wrong again. The Dodd-Frank Act already requires companies to publish the ratios of CEO pay to the pay of the company’s median worker (the Securities and Exchange Commission is now weighing a proposal to implement this). So the California bill doesn’t require companies to do anything more than they’ll have to do under federal law. And the tax brackets in the bill are wide enough to make the computation easy.

What about CEO’s gaming the system? Can’t they simply eliminate low-paying jobs by subcontracting them to another company — thereby avoiding large pay disparities while keeping their own compensation in the stratosphere?

No. The proposed law controls for that. Corporations that begin subcontracting more of their low-paying jobs will have to pay a higher tax.

For the last thirty years, almost all the incentives operating on companies have been to lower the pay of their workers while increasing the pay of their CEOs and other top executives. It’s about time some incentives were applied in the other direction.

The law isn’t perfect, but it’s a start. That the largest state in America is seriously considering it tells you something about how top heavy American business has become, and why it’s time to do something serious about it.

Robert B. Reich has served in three national administrations, most recently as secretary of labor under President Bill Clinton. He also served on President Obama's transition advisory board. His latest book is "Aftershock: The Next Economy and America's Future." His homepage is www.robertreich.org.

'Flash Boys’ by Michael Lewis, ‘Capital in the 21st Century’ by Thomas Piketty

Michael Lewis inhabits a rare place in American culture: Although Lewis doesn’t set agendas, people who read his books can, and do, make things happen. “Flash Boys,” Lewis’s most recent book, is a fiery exploration of the immense manipulative power of high-frequency trading on Wall Street.

Within a week of the book’s publication, the Justice Department, FBI, and State of New York initiated investigations into the practice, all direct responses to the outrage generated by the book.

This is, obviously, remarkable, but the outrage comes easily. As “Flash Boys” amply shows, the purpose of such trading, referred to as HFT, has been to “hardwire into the [stock] exchange’s brain the interests of high-frequency traders – at the expense of everyone who wasn’t a high-frequency trader.”

According to Lewis, HFT crews distort the market to their benefit by “front-running” – the classic, and often illegal, practice of executing stock orders after obtaining early information about other brokers’ order plans. When you front-run the market you buy a stock before your competitor does and then sell it to him or her for more than it would’ve cost if you hadn’t scooped them.

As Lewis writes, “Over the past decade, the financial markets have changed too rapidly for our mental picture of them to remain true to life.” Rather that a bunch of guys on the floor barking orders, the market now operates through boxes of fiber optic cables.

As one of the brokers Lewis writes about says, “People are getting screwed because they can’t imagine a microsecond,” the amount of time it takes to front-run the market if you’re savvy. Yes, it’s microseconds and pennies, but it amounts to billions of dollars in cumulative profits.

Lewis is a smart, inexhaustibly dogged reporter who writes lucid, crystalline prose, often about mind-bogglingly complex topics. Over the course of his career, Lewis has written 15 books, covering topics that include the NFL and baseball statistics. But it’s as a financial reporter that he’s best known, and “Flash Boys” fits firmly in the Lewis-as-financial-demystifier mode.

In Lewis’s telling the explanation and criticism of HFT seem precise. This is Lewis’s cardinal virtue: his ability to take something cripplingly complex and create a distillation, in narrative form, of how complexity tends to shroud and serves something basic. Sins and virtues don’t change. As complex as our world has become, everything serves the same simple goals, such as victory and greed. People don’t evolve at the speed of their tools.

So why has “Flash Boys” become such a flash point? What is it about this book that so threatens to upend the financial world despite years of similar malfeasance? Lewis readily concedes that his book contains little that’s new. Lewis himself writes the “entire history of Wall Street was the story of scandals .*.*. linked together tail to trunk like circus elephants.”

The book asserts a morality in shades of black and white: Lewis sketches heroes and villains, and many of the folks who take umbrage at his portrayal of the market cry foul, claiming that the same dubious practices exist beyond the realm of HFT.

On one hand, this is laudable. When it comes to something as economically powerful as Wall Street, it seems that any time a story prompts long-delayed government oversight, the author is doing something right.

But this fact merely makes the bluster attached to the book that much more interesting. In the dim light of the recent past, can anyone maintain that their anger comes served with a garnish of surprise?

There’s a common assumption that even if you don’t have money, your life in many elemental senses still depends on the stock market. And Lewis’s book is making an impact because a well-told tale about rich people fleecing other, often, richer people speaks to everyone who believes in market essentialism, not merely those who benefit.

The root of the uproar caused by “Flash Boys” is nested in Lewis’s statement that the HFT tactics reveal that the “US stock market [is] now a class system, rooted in speed, of haves and have nots.” In our delusionally “classless” society, this development irritates everyone. Moreover, the outrage over “Flash Boys’’ has triggered action in direct proportion to its vivisection of market perversions that affect the people who matter most in America – the wealthy.

Compare “Flash Boys” with the other big economics-related book of the spring, Thomas Piketty’s “Capital in the 21st Century.” Direct comparison is unfair, of course; Piketty is to Lewis as a lion is to a house cat, at least when it comes to depth of ambition. Piketty, whose previous work we are indebted to for providing statistical verification that the top 1 percent of the population possesses a outsize percentage of wealth, has written a magisterial book about the ever-increasing inequality.

A comprehensive overview of “Capital’s” abundance of historical and analytical data would be impossible here. (Here’s a microreview of Piketty: Read it). In short, Piketty convincingly argues that the world is poised at the threshold of a new gilded age in which the vast majority of wealth is transferred via inheritance. This feels either intuitively right or intuitively wrong, depending on your political predisposition.

Piketty’s genius lies in proving that inequality is growing and potentially threatens widespread political instability. (I should note that my office recently hosted a public event with Piketty). This “has nothing to do with any market imperfection,” Piketty writes. In effect, when the return on capital rises faster than the rate of economic growth, the greater the inequality. This just happens to be what capitalism does.

“Capital” is broad and expansive where “Flash Boys” is laser like and polemical. But that’s not the biggest difference in these books, nor are these reasons why a book like “Flash Boys” ultimately exerts more power over American economic culture. The outrage of “Flash Boys,” at least for those sitting in positions of privilege, is that their return on capital – their investments – are being hijacked by an electronic sleight of hand.

Given that most Americans remain seduced by the market, regulatory reform seems the only option. “Flash Boys” feels like virtue, but it fails to inspect the underlying assumptions and potential, damaging implications of our continued blind reliance on the fiction of “fairness” in any financial and economic system, let alone on Wall Street.

In other words, Piketty has written a trenchant critique of our current economic system while Lewis has written a book about gaming the system. “Flash Boys” is a symptom of the wealth disparity, and the denial of the disparity, that Piketty skewers.

So there are two ways to look at the “Flash Boysâ chatter. As an indictment of Wall Street, it’s highly effective, even great. It’s inspiring that a book like this can catalyze a broad reaction in our culture. But it’s still a book of its time, a time where the vast majority of Americans can’t even get robbed by the people Lewis indicts.

The Meritocracy Myth: How The Super-Rich Really Make Their Money

Warren Buffett once claimed that the “genius of the American economy, our emphasis on a meritocracy and a market system and a rule of law has enabled generation after generation to live better than their parents did.”

The Economist suggested that “people succeed through brains and hard work.” Economist Tyler Cowen believes in a “hyper-meritocracy” in which wealth is created by the most intelligent and motivated people.

That all sounds very inspirational. But the super-rich tend to make their money in less meritorious ways.

1. Betting on Food Prices to Rise Chris Hedges noted that Goldman Sachs’ commodities index “is the most heavily traded in the world. The company hoards rice, wheat, corn, sugar and livestock and jacks up commodity prices around the globe so that poor families can no longer afford basic staples and literally starve.” Numerous sources agree that speculation drives up commodity prices. Wheat, for example, rose in price from $105 to $481 in just eight years.

2. Betting on Mortgages to Fail

In 2007 hedge fund manager John Paulson conspired with Goldman Sachs to create packages of risky subprime mortgages, so that in anticipation of a housing crash he could use other people’s money to bet against his personally designed sure-to-fail financial instruments. His successful bet against American households paid him $3.7 billion.

Adding to the insult is that much of a hedge fund manager’s income is considered carried interest, which is taxed at the lower capital gains rate. How do they merit this? They don’t. As Dean Baker explains, “Carried interest…has no economic rationale. With most other tax breaks there is at least an argument as to how it serves some socially useful purpose.”

3. Renting Houses Back to People Who Lost Them

Private equity firms like Blackstone are buying up foreclosures and renting them back at higher rates while waiting for home prices to rise. As absentee landlords they have little interest in long-term community issues.

They go for even bigger money by packaging the rental agreements into rental-backed securities, which are disturbingly similar to the mortgage-backed securities that brought down the economy in 2008.

4. Being a Banker

Almost all of the big names have participated. HSBC Bank laundered money for Mexican drug cartels. Countrywideand Wells Fargo targeted Blacks and Hispanics for unaffordable subprime loans. GE Capital skimmed billions of dollars from its customers. Bank of America and JP Morgan Chase hid billions of dollars of bonuses and losses and loans from investors. Banks fixed interest rates in the LIBOR scandal, and illegally foreclosed on millions of homeowners in the robo-signing scandal.

5. Making “Can’t Lose” Bets on Wall Street

With high-speedcomputer trading, programs can identify ‘buy’ orders, purchase the stock in a few nanoseconds, and then sell it to the identified buyer for a few pennies more. By doing this millions of times per hour, billions of dollars can be extracted from the stocks that make up our retirement accounts.

Some evidence of the strategy’s effectiveness comes from the astonishing performance of Virtu Financial, which made money in the stock market on 1,277 out of 1,278 days over a five year period. That is, only one bad day in five years.

6. Checking the Stock Portfolio Every Morning

In one year the Forbes 400 ‘earned’ more than the total combined budget for SNAP, WIC (Women, Infants, children), Child Nutrition, Earned Income Tax Credit, Supplemental Security Income, Temporary Assistance for Needy Families, and Housing. These lucky 400 were the main beneficiaries of a stock market that grew by $4.7 trillion in just one year.

7. Having the Right Friends and Relatives

Like having Fred Koch or Sam Walton as your daddy. The authors of The Meritocracy Myth say it well:“In the race to get ahead, the effects of inheritance come first and merit second, not the other way around.”Much of the individual wealth in our country was taken by individuals who had the right connections. The CEOs of Silicon Valley, the alleged mecca of self-made tech visionaries, are no different. A Reuters analysis concluded that a prestigious degree and personal connections to power-brokers are “at least as important as a great idea” for Silicon Valley entrepreneurs.

None of these money-making methods are productive, or praiseworthy, or suggestive of a meritocracy. Perhaps demeritocracy is more appropriate.

10 Things That Everyone Should Know About The Federal Reserve

What would happen if the Federal Reserve was shut down permanently?

That is a question that CNBC asked recently, but unfortunately most Americans don’t really think about the Fed much. Most Americans are content with believing that the Federal Reserve is just another stuffy government agency that sets our interest rates and that is watching out for the best interests of the American people. But that is not the case at all.

The truth is that the Federal Reserve is a private banking cartel that has been designed to systematically destroy the value of our currency, drain the wealth of the American public and enslave the federal government to perpetually expanding debt. During this election year, the economy is the number one issue that voters are concerned about. But instead of endlessly blaming both political parties, the truth is that most of the blame should be placed at the feet of the Federal Reserve.

The Federal Reserve has more power over the performance of the U.S. economy than anyone else does. The Federal Reserve controls the money supply, the Federal Reserve sets the interest rates and the Federal Reserve hands out bailouts to the big banks that absolutely dwarf anything that Congress ever did. If the American people are ever going to learn what is really going on with our economy, then it is absolutely imperative that they get educated about the Federal Reserve.

The following are 10 things that every American should know about the Federal Reserve….

#1 THE FEDERAL RESERVE SYSTEM IS A PRIVATELY OWNED BANKING CARTEL

The Federal Reserve is not a government agency.

The truth is that it is a privately owned central bank. It is owned by the banks that are members of the Federal Reserve system. We do not know how much of the system each bank owns, because that has never been disclosed to the American people.

The Federal Reserve openly admits that it is privately owned. When it was defending itself against a Bloomberg request for information under the Freedom of Information Act, the Federal Reserve stated unequivocally in court that it was “not an agency” of the federal government and therefore not subject to the Freedom of Information Act.

In fact, if you want to find out that the Federal Reserve system is owned by the member banks, all you have to do is go to the Federal Reserve website….

“The twelve regional Federal Reserve Banks, which were established by Congress as the operating arms of the nation’s central banking system, are organized much like private corporations—possibly leading to some confusion about “ownership.” For example, the Reserve Banks issue shares of stock to member banks. However, owning Reserve Bank stock is quite different from owning stock in a private company. The Reserve Banks are not operated for profit, and ownership of a certain amount of stock is, by law, a condition of membership in the System. The stock may not be sold, traded, or pledged as security for a loan; dividends are, by law, 6 percent per year.”

Foreign governments and foreign banks do own significant ownership interests in the member banks that own the Federal Reserve system. So it would be accurate to say that the Federal Reserve is partially foreign-owned.

But until the exact ownership shares of the Federal Reserve are revealed, we will never know to what extent the Fed is foreign-owned.

#2 THE FEDERAL RESERVE SYSTEM IS A PERPETUAL DEBT MACHINE

As long as the Federal Reserve System exists, U.S. government debt will continue to go up and up and up.

This runs contrary to the conventional wisdom that Democrats and Republicans would have us believe, but unfortunately it is true.

The way our system works, whenever more money is created more debt is created as well.

For example, whenever the U.S. government wants to spend more money than it takes in (which happens constantly), it has to go ask the Federal Reserve for it. The federal government gives U.S. Treasury bonds to the Federal Reserve, and the Federal Reserve gives the U.S. government “Federal Reserve Notes” in return. Usually this is just done electronically.

So where does the Federal Reserve get the Federal Reserve Notes?

It just creates them out of thin air.

Wouldn’t you like to be able to create money out of thin air?

Instead of issuing money directly, the U.S. government lets the Federal Reserve create it out of thin air and then the U.S. government borrows it.

Talk about stupid.

When this new debt is created, the amount of interest that the U.S. government will eventually pay on that debt is not also created.

So where will that money come from?

Well, eventually the U.S. government will have to go back to the Federal Reserve to get even more money to finance the ever expanding debt that it has gotten itself trapped into.

It is a debt spiral that is designed to go on perpetually.

You see, the reality is that the money supply is designed to constantly expand under the Federal Reserve system. That is why we have all become accustomed to thinking of inflation as “normal”.

So what does the Federal Reserve do with the U.S. Treasury bonds that it gets from the U.S. government?

Well, it sells them off to others. There are lots of people out there that have made a ton of money by holding U.S. government debt.

In fiscal 2011, the U.S. government paid out 454 billion dollars just in interest on the national debt.

That is 454 billion dollars that was taken out of our pockets and put into the pockets of wealthy individuals and foreign governments around the globe.

The truth is that our current debt-based monetary system was designed by greedy bankers that wanted to make enormous profits by using the Federal Reserve as a tool to create money out of thin air and lend it to the U.S. government at interest.

And that plan is working quite well.

Most Americans today don’t understand how any of this works, but many prominent Americans in the past did understand it.

For example, Thomas Edison was once quoted in the New York Timesas saying the following….

“That is to say, under the old way any time we wish to add to the national wealth we are compelled to add to the national debt. Now, that is what Henry Ford wants to prevent. He thinks it is stupid, and so do I, that for the loan of $30,000,000 of their own money the people of the United States should be compelled to pay $66,000,000 – that is what it amounts to, with interest. People who will not turn a shovelful of dirt nor contribute a pound of material will collect more money from the United States than will the people who supply the material and do the work. That is the terrible thing about interest. In all our great bond issues the interest is always greater than the principal. All of the great public works cost more than twice the actual cost, on that account. Under the present system of doing business we simply add 120 to 150 per cent, to the stated cost. But here is the point: If our nation can issue a dollar bond, it can issue a dollar bill. The element that makes the bond good makes the bill good.”

We should have listened to men like Edison and Ford.

But we didn’t.

And so we pay the price.

On July 1, 1914 (a few months after the Fed was created) the U.S. national debt was 2.9 billion dollars.

Today, it is more than more than 5000 times larger.

Yes, the perpetual debt machine is working quite well, and most Americans do not even realize what is happening.

#3 THE FEDERAL RESERVE HAS DESTROYED MORE THAN 96% OF THE VALUE OF THE U.S. DOLLAR

Did you know that the U.S. dollar has lost 96.2 percent of its value since 1900? Of course almost all of that decline has happened since the Federal Reserve was created in 1913.

Because the money supply is designed to expand constantly, it is guaranteed that all of our dollars will constantly lose value.

Inflation is a “hidden tax” that continually robs us all of our wealth. The Federal Reserve always says that it is “committed” to controlling inflation, but that never seems to work out so well.

And current Federal Reserve Chairman Ben Bernanke says that it is actually a good thing to have a little bit of inflation. He plans to try to keep the inflation rate at about 2 percent in the coming years.

So what is so bad about 2 percent? That doesn’t sound so bad, does it?

Well, just consider the following excerpt from a recent Forbes article….

“The Federal Reserve Open Market Committee (FOMC) has made it official: After its latest two day meeting, it announced its goal to devalue the dollar by 33% over the next 20 years. The debauch of the dollar will be even greater if the Fed exceeds its goal of a 2 percent per year increase in the price level.”

#4 THE FEDERAL RESERVE CAN BAIL OUT WHOEVER IT WANTS TO WITH NO ACCOUNTABILITY

The American people got so upset about the bailouts that Congress gave to the Wall Street banks and to the big automakers, but did you know that the biggest bailouts of all were given out by the Federal Reserve?

Thanks to a very limited audit of the Federal Reserve that Congress approved a while back, we learned that the Fed made trillions of dollars in secret bailout loans to the big Wall Street banks during the last financial crisis. They even secretly loaned out hundreds of billions of dollars to foreign banks.

According to the results of the limited Fed audit mentioned above, a total of $16.1 trillion in secret loans were made by the Federal Reserve between December 1, 2007 and July 21, 2010.

The following is a list of loan recipients that was taken directly from page 131 of the audit report….

Citigroup - $2.513 trillion

Morgan Stanley - $2.041 trillion

Merrill Lynch - $1.949 trillion

Bank of America - $1.344 trillion

Barclays PLC - $868 billion

Bear Sterns - $853 billion

Goldman Sachs - $814 billion

Royal Bank of Scotland - $541 billion

JP Morgan Chase - $391 billion

Deutsche Bank - $354 billion

UBS - $287 billion

Credit Suisse - $262 billion

Lehman Brothers - $183 billion

Bank of Scotland - $181 billion

BNP Paribas - $175 billion

Wells Fargo - $159 billion

Dexia - $159 billion

Wachovia - $142 billion

Dresdner Bank - $135 billion

Societe Generale - $124 billion

“All Other Borrowers” - $2.639 trillion

So why haven’t we heard more about this?

This is scandalous.

In addition, it turns out that the Fed paid enormous sums of money to the big Wall Street banks to help “administer” these nearly interest-free loans….

“Not only did the Federal Reserve give 16.1 trillion dollars in nearly interest-free loans to the “too big to fail” banks, the Fed also paid them over 600 million dollars to help run the emergency lending program. According to the GAO, the Federal Reserve shelled out an astounding $659.4 million in “fees” to the very financial institutions which caused the financial crisis in the first place.”

Does reading that make you angry?

It should.

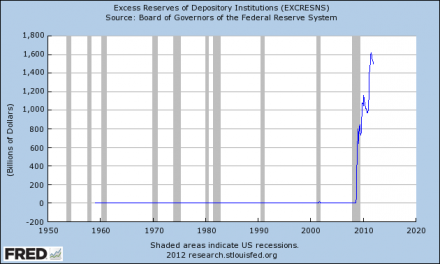

#5 THE FEDERAL RESERVE IS PAYING BANKS NOT TO LEND MONEY

Did you know that the Federal Reserve is actually paying banks not to make loans?

It is true.

Section 128 of the Emergency Economic Stabilization Act of 2008 allows the Federal Reserve to pay interest on “excess reserves” that U.S. banks park at the Fed.

So the banks can just send their cash to the Fed and watch the money come rolling in risk-free.

So are many banks taking advantage of this?

You tell me. Just check out the chart below. The amount of “excess reserves” parked at the Fed has gone from nearly nothing to about 1.5 trillion dollars since 2008….

But shouldn’t the banks be lending the money to us so that we can start businesses and buy homes?

You would think that is how it is supposed to work.

Unfortunately, the Federal Reserve is not working for us.

The Federal Reserve is working for the big banks.

Sadly, most Americans have no idea what is going on.

Another example of this is the government debt carry trade.

Here is how it works. The Federal Reserve lends gigantic piles of nearly interest-free cash to the big Wall Street banks, and in turn those banks use the money to buy up huge amounts of government debt. Since the return on government debt is higher, the banks are able to make large profits very easily and with very little risk.

This scam was also explained in a recent article in the Guardian….

“Consider this: we pretend that banks are private businesses that should be allowed to run their own affairs. But they are the biggest scroungers of public money of our time. Banks are lent vast sums of money by central banks at near-zero interest. They lend that money to us or back to the government at higher rates and rake in the difference by the billion. They don’t even have to make clever investments to make huge profits.”

That is a pretty good little scam they have got going, wouldn’t you say?

#6 THE FEDERAL RESERVE CREATES ARTIFICIAL ECONOMIC BUBBLES THAT ARE EXTREMELY DAMAGING

By allowing a centralized authority such as the Federal Reserve to dictate interest rates, it creates an environment where financial bubbles can be created very easily.

Over the past several decades, we have seen bubble after bubble. Most of these have been the result of the Federal Reserve keeping interest rates artificially low. If the free market had been setting interest rates all this time, things would have never gotten so far out of hand.

For example, the housing crash would have never been so horrific if the Federal Reserve had not created such ideal conditions for a housing bubble in the first place. But we allow the Fed to continue to make the same mistakes.

Right now, the Federal Reserve continues to set interest rates much, much lower than they should be. This is causing a tremendous misallocation of economic resources, and there will be massive consequences for that down the line.

#7 THE FEDERAL RESERVE SYSTEM IS DOMINATED BY THE BIG WALL STREET BANKS

Even since it was created, the Federal Reserve system has been dominated by the big Wall Street banks.

The following is from a previous article that I did about the Fed….

“The New York representative is the only permanent member of the Federal Open Market Committee, while other regional banks rotate in 2 and 3 year intervals. The former head of the New York Fed, Timothy Geithner, is now U.S. Treasury Secretary. The truth is that the Federal Reserve Bank of New York has always been the most important of the regional Fed banks by far, and in turn the Federal Reserve Bank of New York has always been dominated by Wall Street and the major New York banks.”

#8 IT IS NOT AN ACCIDENT THAT WE SAW THE PERSONAL INCOME TAX AND THE FEDERAL RESERVE SYSTEM BOTH COME INTO EXISTENCE IN 1913

On February 3rd, 1913 the 16th Amendment to the U.S. Constitution was ratified. Later that year, the United States Revenue Act of 1913imposed a personal income tax on the American people and we have had one ever since.

Without a personal income tax, it is hard to have a central bank. It takes a lot of money to finance all of the government debt that a central banking system creates.

It is no accident that the 16th Amendment was ratified in 1913 and the Federal Reserve system was also created in 1913.

They have a symbiotic relationship and they are designed to work together.

We could fill Congress with people that are committed to ending this oppressive system, but so far we have chosen not to do that.

So our children and our grandchildren will face a lifetime of debt slavery because of us.

I am sure they will be thankful for that.

#9 THE CURRENT FEDERAL RESERVE CHAIRMAN, BEN BERNANKE, HAS A NIGHTMARISH TRACK RECORD OF INCOMPETENCE

The mainstream media portrays Federal Reserve Chairman Ben Bernanke as a brilliant economist, but is that really the case?

Let’s go to the videotape.

In 2005, Bernanke said that we shouldn’t worry because housing prices had never declined on a nationwide basis before and he said that he believed that the U.S. would continue to experience close to “full employment”…. “We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though.”

In 2005, Bernanke also said that he believed that derivatives were perfectly safe and posed no danger to financial markets…. “With respect to their safety, derivatives, for the most part, are traded among very sophisticated financial institutions and individuals who have considerable incentive to understand them and to use them properly.”

In 2006, Bernanke said that housing prices would probably keep rising…. “Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise.”

In 2007, Bernanke insisted that there was not a problem with subprime mortgages…. “At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.”

In 2008, Bernanke said that a recession was not coming…. “The Federal Reserve is not currently forecasting a recession.”

A few months before Fannie Mae and Freddie Mac collapsed, Bernanke insisted that they were totally secure…. “The GSEs are adequately capitalized. They are in no danger of failing.”

For many more examples that demonstrate the absolutely nightmarish track record of Federal Reserve Chairman Ben Bernanke, please see the following articles….

But after being wrong over and over and over, Barack Obama still nominated Ben Bernanke for another term as Chairman of the Fed.

#10 THE FEDERAL RESERVE HAS BECOME WAY TOO POWERFUL

The Federal Reserve is the most undemocratic institution in America.

The Federal Reserve has become so powerful that it is now known as “the fourth branch of government”, but there are less checks and balances on the Fed than there are on the other three branches.

The Federal Reserve runs the U.S. economy but it is not accountable to the American people. We can’t vote those that run the Fed out of office if we do not like what they do.

Yes, the president appoints those that run the Fed, but he also knows that if he does not tread lightly he won’t get the money from the big Wall Street banks that he needs for his next election.

Thankfully, there are a few members of Congress that are complaining about how much power the Fed has. For example, Ron Paul once told MSNBC that he believes that the Federal Reserve is now actually more powerful than Congress…..

“The regulations should be on the Federal Reserve. We should have transparency of the Federal Reserve. They can create trillions of dollars to bail out their friends, and we don’t even have any transparency of this. They’re more powerful than the Congress.”

As members of Congress such as Ron Paul have started to shed some light on the activities of the Federal Reserve, that has caused many in the mainstream media to come to the defense of the Fed.

For example, a recent CNBC article entitled “If The Federal Reserve Is Abolished, What Then?” makes it sound like there is absolutely no other rational alternative to having the Federal Reserve run our economy.

But this is not what our founders intended.

The founders did not intend for a private banking cartel to issue our money and set our interest rates for us.

According to Article I, Section 8 of the U.S. Constitution, the U.S. Congress has been given the responsibility to “coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures”.

So why is the Federal Reserve doing it?

But the CNBC article mentioned above makes it sound like the sky would fall if control of the currency was handed back over to the American people.

At one point, the article asks the following question….

“How would the U.S. economy then function? Something has to take its place, right?”

No, the truth is that we don’t need anyone to “manage” our economy.

The U.S. Treasury could be in charge of issuing our currency and the free market could set our interest rates.

We don’t need to have a centrally-planned economy.

We aren’t China.

And it goes against everything that our founders believed to be running up so much government debt.

“I wish it were possible to obtain a single amendment to our Constitution. I would be willing to depend on that alone for the reduction of the administration of our government to the genuine principles of its Constitution; I mean an additional article, taking from the federal government the power of borrowing.”

Oh, how things would have been different if we had only listened to Thomas Jefferson.

Please share this article with as many people as you can. These are things that every American should know about the Federal Reserve, and we need to educate the American people about the Fed while there is still time.

A lack of transparency allows financial firms to conceal what they do with your money.

In the national debate over what to do about public pension shortfalls, here's something you may not know: The texts of the agreements signed between those pension funds and financial firms are almost always secret. Yes, that's right. Although they are public pensions that taxpayers contribute to and that public officials oversee, the exact terms of the financial deals being engineered in the public's name and with public money are typically not available to you, the taxpayer.

To understand why that should be cause for concern, ponder some possibilities as they relate to pension deals with hedge funds, private equity partnerships and other so-called "alternative investments." For example, it is possible that the secret terms of such agreements could allow other private individuals in the same investments to negotiate preferential terms for themselves, meaning public employees' pension money enriches those private investors. It is also possible that the secret terms of the agreements create the heads-Wall-Street-wins, tails-pensions-lose effect -- the one whereby retirees' money is subjected to huge risks, yet financial firms' profits are guaranteed regardless of returns.